Economic Definition of Change in Supply

Change in Supply

View FREE Lessons!

Definition of Change in Supply:

A change in supply is a change in the quantity of a good or service businesses are willing to produce at every price, as illustrated by a shift in the entire supply curve.

Detailed Explanation:

Profits increase when a company's cost to produce and deliver a good or service decreases. Because lower manufacturing costs increase profits, companies are willing to increase production, even if there is no change in the price. Conversely, manufacturers would reduce the supply of goods and services following an increase in their cost to produce a product if there is no change in its price. Any event that changes a company's cost to manufacture a good or service will cause a change in the supply of that good or service.Technological advances, lower input costs, tax cuts, subsidies, and more lenient regulations reduce a manufacturer's cost and induce them to raise their level of production. Conversely, higher input prices, tax increases, and costly regulations increase costs and reduce supply.

Factors other than a direct cost such as the cost of other products can also influence businesses to alter their production. Maximizing the expected profit remains the motivation for the change in supply. For example, farmers may choose to substitute corn for soybeans if the price of corn increases. The opportunity cost of planting soybeans has increased, so farmers plant fewer acres of soybeans and more of corn. The entry and exit of firms into an industry change the market supply. Political disruptions and natural disasters may also impact supply.

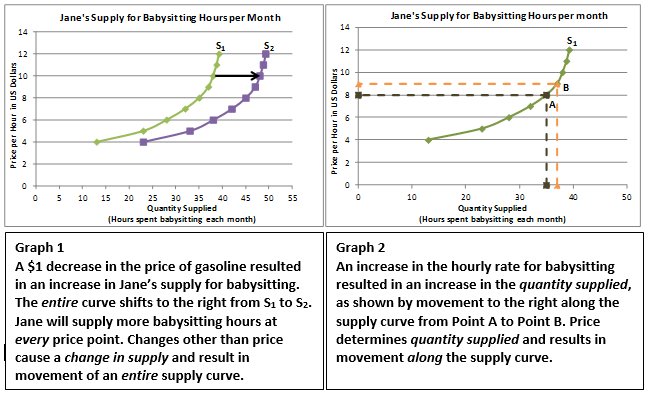

Suppliers are also willing to increase production at higher prices, ceteris paribus. This results in an increase in the quantity supplied, rather than an increase in the supply. Changes in quantity supplied are represented graphically by movement along the existing supply curve. A change in supply causes the entire supply curve to shift. To illustrate the distinction between a change in the supply and a change in the quantity supplied assume the price of gasoline decreases by $1.00 a gallon. Jane the babysitter is thrilled. She can now expand her market since it is less expensive to travel to clients' homes. Her supply curve shifts to the right. Jane would be willing to increase the number of hours she babysits at every price along the supply curve. This is shown in Graph 1 below. Prior to the decrease in gas prices, she was willing to babysit 35 hours per month at $8.00 an hour. After the drop in gas prices, she is willing to babysit 45 hours a month without increasing her fee. This differs from her willingness to increase the number of hours she babysits if she is able to raise her price. In this case, we have movement along the supply curve. For example, if Jane could charge $9.00 an hour she would be willing to babysit 37 hours per month. This is illustrated in Graph 2.

An easy test in identifying whether there would be a change in supply or a change in the quantity supplied is to ask, "Would a producer change the amount supplied if there is no change in price?". If the answer is "Yes", then there would be a change in the supply. "No" means there is a change in the quantity supplied. Increases in supply cause the curve to shift to the right, while decreases cause it to shift to the left.

Here is a brief video explaining changes in supply in the mortgage industry between 1982 and 2010.

Dig Deeper With These Free Lessons:

Changes in Supply – When Producer Costs Change

Changes in Demand – When Consumer Tastes Change

Supply – The Producer's Perspective

Price Elasticity of Supply – How Does A Producer Respond to a Price Change

Supply and Demand – Producers and Consumers Reach Agreement

Economic Definition of Change in Supply

Source: https://www.higherrockeducation.org/glossary-of-terms/change-in-supply

0 Response to "Economic Definition of Change in Supply"

Post a Comment